Amidst renewed whisperings of an impending recession in the second half of 2023 and the possibility of a debt default by the U.S. government that could trigger unemployment and surging interest rates, importers and logistics service providers (LSPs) are bracing for a potential hard landing. On balance, however, there are signs that a number of the challenges to global supply chain performance in 2023 are abating.

BIG GAINS IN IMPORT VOLUMES

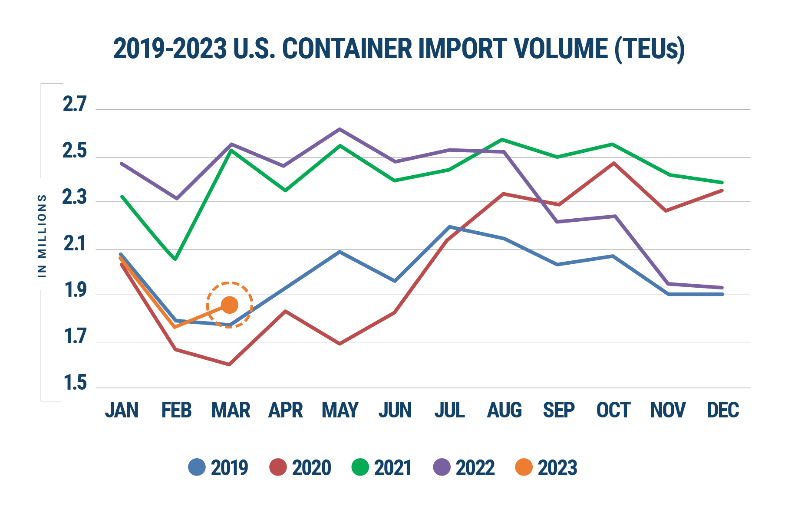

Partly driven by a spike in imports from China, U.S. container import volumes increased significantly in April 2023, rising 9% from March 2023 (Figure 1). Although container volume was down 17.8% from April 2022, imports were up 5.3% from pre-pandemic April 2019 and are continuing to track to 2019 levels—an encouraging trend.

Figure 1: U.S. Container Import Volume Year-over-Year Comparison

In a dramatic reversal of its downward trend, Chinese imports into the U.S. increased 26.7% in April 2023 compared to March volumes—representing 82% of the total volume increase from the top 10 countries importing into the U.S—although still down 26% from the August 2022 high. Compared to March 2023, April import volumes from Hong Kong (24.4%), Taiwan (19.3%), and Vietnam (13.8%) also increased significantly. In April 2023, China represented 36.8% of the total U.S. box imports, an increase of 5.2% from March, but still 4.7% below the high of 41.5% in February 2022.

PORT PERFORMANCE IMPROVING

In April 2023, U.S. container import volume at the top 10 ports increased 167,174 TEUs from March levels, with the Port of New York/New Jersey showing the greatest overall container volume increase (54,466 TEUs), followed by the Port of Savannah (24,923 TEUs). Given that the dramatic increase of Chinese imports in April should have favored West Coast ports, this growth pattern is somewhat counterintuitive.

Notably, despite the increased activity, port delays declined significantly at all of the top ports (Figure 2). Signaling that global supply chain challenges are subsiding, port transit times were at their lowest level since 2021.

Figure 2: Monthly Average Transit Delays (in days) for the Top 10 Ports

Note: Descartes’ definition of port transit delay is the difference as measured in days between the Estimated Arrival Date, which is initially declared on the bill of lading, and the date when Descartes receives the CBP-processed bill of lading.

CHALLENGES EASING

Importers and LSPs will be relieved that the two sides in the International Longshore and Warehouse Union (ILWU) and Pacific Maritime Association (PMA) negotiations are inching towards a new contract. Talks have been dragging on since May 2022 (the contract expired July 1, 2022) but PMA and the union have reached agreement on “certain key issues.” However, PMA commented that several important issues remain unresolved and work actions led by ILWU Local 13 at the Ports of Los Angeles and Long Beach continue to disrupt some operations at key marine terminals.

While some major shippers have been diverting cargo from the West Coast to ports on the East Coast and Gulf of Mexico to avoid potential work stoppages, there has been no serious impact on container processing, as has occurred in the past. The final resolution of the contract could bring some Asia-originating containers that had shifted to rival ports back to major California ports to take advantage of the shorter transit times.

While energy prices are generally moving in the right direction, fuel costs remain elevated, exerting continued pressure on the transportation budgets of importers and LSPs. The price of gasoline—a significant contributor to high inflation rates—increased slightly to $3.60/gallon but was down $0.58/gallon from the same time in 2022, according to the U.S. Energy Information Administration.

Diesel costs also fell slightly to $4.02/gallon, a $1.49/gallon drop from April 2022. While declining fuel costs is always good news for logistics and supply chain companies, gasoline and diesel prices are likely to remain elevated for the foreseeable due to the disruption of global energy markets caused by the war in Ukraine and follow-on sanctions against Russia.

MANAGING SUPPLY CHAIN RISK

Although recent developments appear to indicate an easing of supply chain turbulence, importers and LSPs should keep an eye on several factors and ongoing issues that could cause further disruptions, tailoring their logistics and supply chain strategies accordingly to mitigate risk and promote financial stability.

1. Union issues and labor laws:

Logistics companies should closely monitor the progress of the IWLU-PMA contract negotiations. Progress is tediously slow but movement in either direction will impact port performance and the ability of importers to efficiently move their goods where they need to go. In addition, California’s AB5 legislation has the potential to cause more disruption at California’s port operations.

2. Port activity:

Importers and LSPs need to keep a close eye on import volumes and port transit times. Recent U.S. container imports are continuing to align with 2019 volumes but, if monthly TEU volumes surge to between 2.4M and 2.6M, as witnessed during the pandemic, ports and inland logistics would be under significant strain.

Logistics companies should continue to seek out less congested transportation lanes, including smaller ports, to improve supply chain velocity and reliability. Evaluating alternative transportation lanes into the U.S., including entry through northern and southern borders and inland ports, is also a smart strategy to allay risk.

If port transit times decrease, as they did in April, it’s an indication that the efficiency of global supply chain capabilities has improved or, alternatively, that the demand for goods and logistics services is declining. Either way, pressure on the ports is relieved—good news for logistics-oriented companies.

3. Russia/Ukraine war and inflation

Importers and LSPs should monitor the ongoing impact of the Russia/Ukraine conflict on their logistics costs and capacity constraints, while ensuring that their key trading partners are not on sanctions lists.

On the economic front, the latest Consumer Price Index report available (March 2023) showed a continuing decline in inflation, but the inflation rate remains elevated. Fuel prices—inextricably linked to inflation and a major component of logistics companies’ operational costs—should be monitored closely. Given that fuel prices will remain elevated indefinitely due to the war, logistics companies should evaluate ways to increase the fuel efficiency of their fleets, such as route optimization software or alternative-fuel vehicles.

4. Ongoing pandemic impacts

While WHO recently declared that Covid-19 no longer represents a global health emergency—and the U.S. followed suit, terminating its federal COVID-19 Public Health Emergency act—the pandemic continues to impact global supply chain performance, especially in China. In fact, a 2023 analyst report declared that sourcing from Chinese manufacturers is tied to the largest supply chain risks; the possibility of delays and cancellations from Chinese suppliers is high due to the likelihood of COVID-19 localized disruptions in the country.

FINAL THOUGHTS

The good news is that the pressure on supply chains and logistics operations is continuing to ease. However, we’re not in the clear just yet. Several challenges—from labor issues, elevated fuel prices, and economic uncertainty to the impact of the war in Ukraine and the lingering pandemic-related disruptions—continue to stress logistics operations. But by proactively monitoring key supply chain performance and economic indicators, importers and LSPs can address any capacity constraints or supply chain disruptions that may arise in the short term, while building long-term supply chain resilience to mitigate risk in the latter half of 2023 and beyond.