As the new year unfolds, importers and logistics service providers (LSPs) are experiencing signs of relief from the logistical challenges of the past couple years, with U.S. container imports falling back in line with 2019 levels and port wait times continuing to decrease. On the flip side, key economic indicators, such as employment and inflation, paint a conflicting picture of their future impact on import volumes. Combined with COVID uncertainty, geopolitical upheaval, and ongoing U.S. West Coast labor issues, macroeconomic indicators point to further disruptions and challenging global supply chain performance in 2023.

IMPORT VOLUMES APPROACHING PRE-PANDEMIC LEVELS

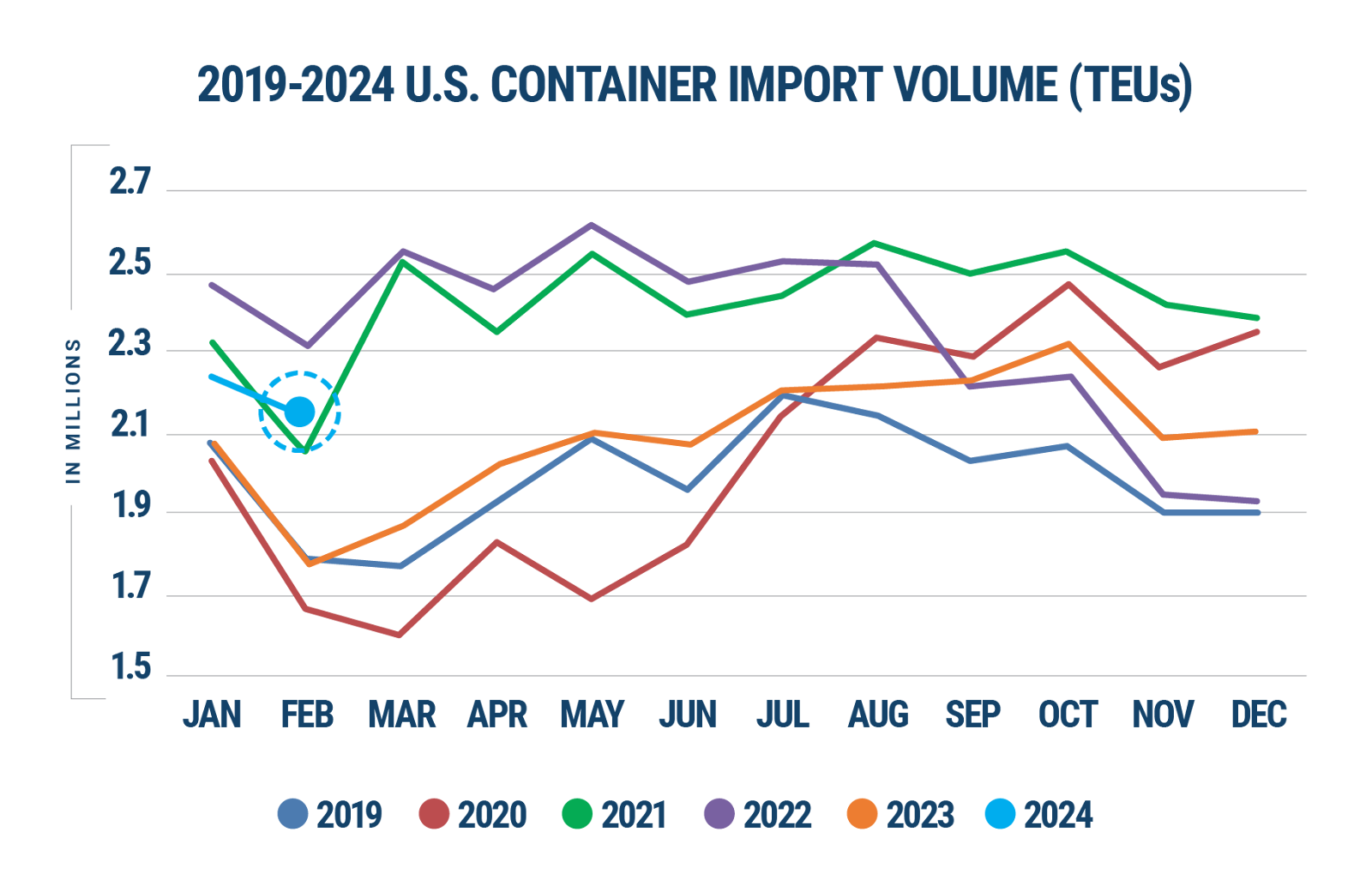

When the global pandemic took hold in 2020, the “Stuff Economy” flourished, with consumer demand for apparel, kitchen appliances, sports equipment, and other retail goods soaring to unforeseen heights. U.S. imports accelerated in kind, precipitating a complex and unprecedented global supply chain crisis. Yet in the latter months of 2022, as record inflation took a bite out of disposable income and consumers put Covid in their rear-view mirror, shifting spending away from the purchase of goods towards services (e.g., travel, restaurants, entertainment), U.S. container imports began to decline.

Recent data shows December 2022 U.S. container imports receding to pre-pandemic 2019 levels. Indeed, December volumes declined 1.3% from November to 1,929,032 TEUs (see Figure 1). Although the holiday season in the second half of the month can adversely impact December import volumes, TEU volume was down 19.3% compared to December 2021—and sat just 1.3% higher than December 2019, before the pandemic forced lockdowns and sent the global supply chain into a tailspin.

Figure 1: U.S. Container Import Volume Year-over-Year Comparison

Source: Descartes Datamyne™

WEST COAST PORTS GAIN MARKET SHARE

While overall import volume decreased, half of the top 10 U.S. ports saw volume increases. The Port of Los Angles returned to its position as the top container import processing port, importing 349,493 TEUs and reporting the greatest increase, while the Ports of Houston and New York/New Jersey experienced the greatest drop in total import volume, declining 37,611 and 28,206 TEUs, respectively (see Figure 2).

Figure 2: November to December Comparison of Import Volumes at Top 10 U.S. Ports

Source: Descartes Datamyne™

In December 2022, top West Coast ports reversed their market share decline. Comparing the top five West Coast ports to the top five East and Gulf Coast ports in December vs. November, the total import container volume of West Coast ports grew to 38.1% in December. This gain represents a 1.2% increase from the previous month. In contrast, volume at East and Gulf Coast ports declined in December to 45.5%, down 1.7% from November.

Despite this market share reversal, the top West Coast ports continued to experience container throughput shifts to other ports, including East and Gulf Coasts, from August through December 2022. However, with the exception of the Port of Houston, the top East and Gulf Ports are now operating below the peak volume levels that drove port congestion in 2021.

PORT VELOCITY INCREASING

In good news for importers and LSPs, port delays continued to decline in December, especially for East Coast ports which saw a sizeable decrease and reported no double-digit wait times. Major West Coast ports are all now well below 10 days wait times and have somewhat stabilized. Much of this progress can be attributed to the continued reduction in volume that the majority of ports have experienced in the latter months of 2022.

While wait times have made significant progress, schedule reliability still remains low when compared to pre-pandemic numbers. According to a recent Sea-Intelligence report, schedule reliability is almost 20% lower than in 2019.

CONTINUING IMPACT OF THE PANDEMIC: CHINA FOCUS

More than two years in, the spread of COVID subvariants continues to add uncertainty to the trajectory of the pandemic, impacting supply chains and global trade in unpredictable ways. While China relaxed its “zero-Covid” policy in early December in an effort to spur growth, the country’s exports continue to drop, with December’s 9.9% contraction the worst since February 2020, as China now grapples with the fallout, economic and otherwise, of the highly contagious Omicron variant.

With Lunar New Year—arguably the most important holiday of the year in China—beginning January 22, hundreds of millions of Chinese workers will be traveling in the midst of an Omicron wave. This has the potential to lead to localized lockdowns that could impede workers’ travel home to their manufacturing jobs, shortages of quarantine space in factory cities, and further disruptions in manufacturing and supply chain operations.

Of note, the downward trend of U.S. container imports from China continued in December, falling to 686,514 TEUs—down 0.5% from November and 31.9% from the 2022 high in August. Overall, China represented 35.4% of the total U.S. container imports, a decline of 6.1% from the high of 41.5% in February 2022. By comparison, U.S. imports showed strong growth from Japan and Thailand, increasing by 10.6% and 9.1%, respectively.

KEEP AN EYE ON LABOR AND INFLATION IN 2023

While members of the International Longshore and Warehouse Union (ILWU) have been working without a contract since July 1, 2022, the more pressing concern is California’s AB5 legislation which could lead to more port terminal shutdowns. This continuing labor uncertainty may be a significant reason why import volumes are not shifting back to major California ports, despite their improving situation.

Importers and LSPs should watch the progress of the ILWU contract negotiations and monitor the impact of AB5 on owner-operators serving California ports for potential disruption or any degradation of port container processing performance.

Heading into 2023 with the threat of a global recession looming, key indicators offer a mixed view of the U.S. economy and, ultimately, demand for imports. Inflation remained high in December and, although both diesel and gas prices softened, they are likely to remain elevated for the foreseeable future due to the disruption of global energy markets driven by the war in the Ukraine and subsequent sanctions against Russia.

While inflation may be the only way to slow down the strong U.S. economy and, ultimately, help to alleviate existing global logistics capacity-related challenges, consumer spending remained relatively steady (up 0.1% in November) and the strong December job numbers—employment increased by 223,000 jobs and unemployment declined to record levels at 3.5%—are still contrary to the expected negative impact of high inflation figures and fuel prices. Of concern, strong employment numbers can put pressure on labor-intensive supply chain and logistics operations, impeding the ability to ensure adequate resources to meet customer demand.

PARTING THOUGHTS

Overall, December U.S. container import data points to less pressure on supply chains and logistics operations. While pre-pandemic volume levels do offer a degree of relief from the logistical challenges that have plagued operations for the past few years, a number of issues may cause further disruptions this year. Outbreak risks from new Covid variants, geopolitical conflicts including Russia’s war in the Ukraine, ongoing labor negotiations at busy West Coast ports, and the threat of global recession are all on the radar of importers and LSPs. By keeping a close eye on these factors, in conjunction with key economic indicators—inflation rate, monthly BLS Jobs Report, FRED Inventory to Sales Ratio and FRED Personal Consumption Expenditure: Durable Goods—importers and LSPs can mitigate risk and heighten supply chain reliability to bolster their bottom line in the face of 2023’s uncertainties.