Container xChange, an online container logistics platform, published its August Container Market Forecaster today. Despite the ongoing market fluctuations, the Container Price Sentiment Index (xCPSI) has exhibited resilience and witnessed growth in July as compared to the month of June. The forecaster also noted that container prices have been relatively stable over the past 30 days (July) as compared to the previous 90 days (May-July).

The Container Price Sentiment Index (xCPSI) conducts market surveys concurrently and distils industry experts’ collective insights about container price trends into a quantitative measure, providing insight into near-future expectations for the container market dynamics. In July, 2,570 supply chain professionals participated in the survey.

While the opinion is varied, still most respondents (42%) foresee an increase in container prices in the near-term which is indicative of potential market improvement, 28% foresee a further decline in container prices, suggesting a certain degree of pessimism in market conditions. 30% of those surveyed maintained that prices would remain unchanged.

This growth in sentiment underscores the industry’s anticipation of an imminent turnaround, contributing a sense of positivity to the landscape.

Container Industry Stabilizing Amidst Market Fluctuations

Average container prices have been relatively stable in the last 30 days as compared to the price volatility over the past 90 days (30 days – July, 90 days – May-July).

Analyzing a 30-day price delta comparison across key regions, the market has witnessed average price fluctuations ranging from -4% to +5.20% in the month of July 2023. However, the container prices have experienced a visible dip over a 90-day period, with Southeast Asia reporting a substantial -15.73% decline from May to July 2023.

Despite this sustained dip, the sentiment index has stayed strong, even growing in July. The alignment of sentiment and pricing trends suggests an industry outlook that foresees a turning point, shifting away from skepticism towards a shared anticipation of market recovery despite ongoing price adjustments.

Asian ports have been witnessing steady changes in average container prices for 40 HC cargo-worthy containers. For shippers, engaging in container trading or leasing within Southeast Asia at present, compared to three months prior or even just one month ago, presents a viable business prospect.

These average prices for 20 ft cargo worthy containers (region-wise) as of 9th August 2023 is illustrated in the graph below.

Carrier Capacity Management Spur Intra-Asia Trade Surge

According to Fitch Ratings, in the second quarter of 2023, China witnessed a 6% year on year increase in total container throughput, a significant improvement compared to 3% growth in first quarter of 2023. This expansion was primarily propelled by intensification of trade under the Regional Comprehensive Economic Partnership (RCEP), introduction of new foreign trade routes at the Dalian port, and upward trajectory of trade with nations participating in the Belt and Road Initiative.

A surge in demand for containers on Intra Asia trade lanes was observed on the platform, for example, the China to India stretch was popular in the month of July on Container xChange.

Here are the top five stretches for both the 40 HC and 20 DC containers Ex China on xChange Insights as on 10th August 2023 –

| 40 ft HC | 20 ft DC |

| China to India | China to United States |

| China to Russian Federation | China to India |

| China to China | China to Russian Federation |

| China to United Arab Emirates | China to Canada |

| China to Belarus | China to United Arab Emirates |

Leasing charges for 40 ft HC containers on stretches Ex-China are amongst the top 10 stretches on xChange Insights indicating a bounce back from low leasing pick up charges over the last months.

Indications from Drewry point towards Asia’s entry into a peak season, resulting in a notable 42% surge in the Shanghai-Los Angeles spot rate over a four-week period concluding on August 3rd. Simultaneously, the Drewry Shanghai-Rotterdam index also saw a 20% upswing within the same duration.

Due to increased trade between India and the wider Asian region, ocean carriers are adding more capacity on the Intra-Asia trade route. This is also propelled by the sourcing diversification strategy in South Asia, particularly in countries like Vietnam and India. The aim is to increase shipment volumes and improve market presence. These changes in strategy allow these companies to optimise their operations and potentially strengthen their market position. This is important in a dynamic and competitive shipping industry.

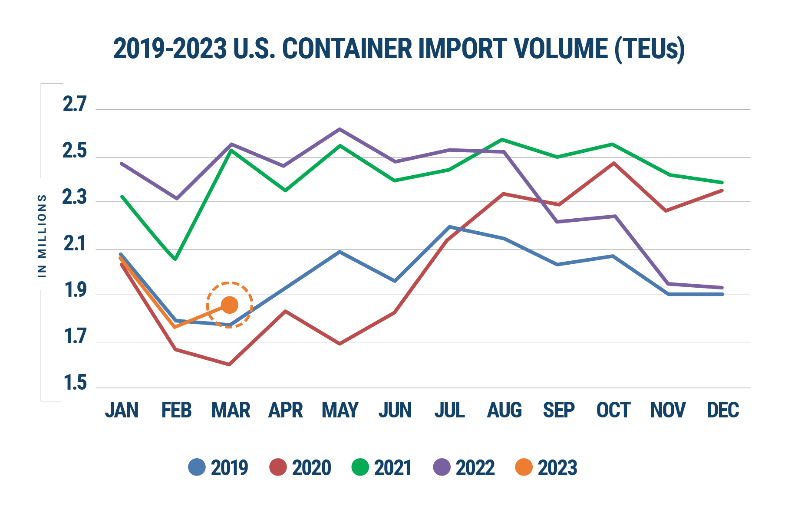

United States: A potential Industry Rebound

The Global Ports Tracker forecasts, provided by NRF (National Retail Federation), indicate that import cargo volumes are poised to reach their peak in August 2023. This surge aligns with retailers’ preparations for the winter holiday season stocking.

Real GDP increased at an annual rate of 2.4% for the April-through-June period, after rising 2% in the first quarter this year, surpassing expectations and delaying concerns of a recession.

The S&P Global Flash US Manufacturing PMI posted 49.0 in July, up from 46.3 in June indicates market improvement. A decrease of 0.5% in wholesale inventories also indicates that the inventories are becoming leaner in the US.

“As economists shift from predicting recession to a ‘soft landing’, the industry holds its momentum. While some experts remain cautious, the foundation of a resilient economy, sustained consumer activity, and strategic federal investments improves the outlook of the upcoming holiday season.” shared Christian Roeloffs, cofounder and CEO, Container xChange.

“It’s a shipper’s market this peak season as rates stabilize at below pre-COVID levels and capacity is abundant. Prices are low and this offers a great opportunity for exporters this peak season.” Roeloffs added.

Eurozone Emerges from Technical Recession: A Turning Tide

In the second quarter of 2023, seasonally adjusted GDP increased by 0.3% in the euro area and was stable in the EU, compared with the previous quarter, according to a preliminary flash estimate published by Eurostat, the statistical office of the European Union. In the first quarter of 2023, GDP had remained stable in the euro area and had increased by 0.2% in the EU. Therefore, avoiding a technical recession in Eurozone.

“Although we did avoid a technical recession in the Eurozone, retail trade is down by 0.3%, along with high inflation rate. These high prices will continue to exert pressure on operating costs for shipping companies. Carriers and freight forwarders should anticipate rising expenses related to provisioning ships and providing for crew members. Shippers might also experience increased costs for transporting goods, affecting overall supply chain costs.” Commented Roeloffs.

“Short-term shipping demand may experience a boost, especially for routes connected to countries with stronger growth rates like Ireland and Spain. However, the potential for growth to be less robust than expected warrants cautious optimism. Prepare for potential shifts in shipping demand as companies explore more cost-efficient transport options during uncertain economic periods.” Added Roeloffs.

The shipping industry’s course for the next few months is intricately woven with economic shifts, trade dynamics, and supply chain adaptations. As we approach the holiday season, the industry’s resilience and adaptability will be put to the test.