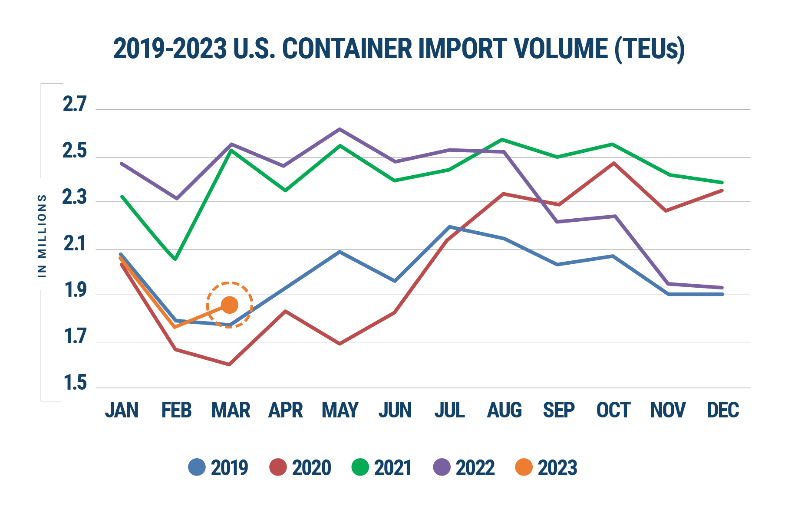

The automotive industry struggled to meet demand during the pandemic as global supply chain congestion and parts shortages left lots empty. Dealers and manufacturers are now rebounding to meet pent-up demand and drive sales after a tough 2022. In fact, S&P Global Mobility expects new vehicle sales globally to reach nearly 83.6 million units in 2023, a 5.6% increase from last year.

Economic challenges could impact this growth, but as automakers are bouncing back, now is a good time to take a holistic look at supply chain strategies to help reduce costs, emissions, and delays.

Reflecting on the past few years, the auto industry is a great example of why supply chains must regularly be optimized in a holistic way. The supply chain strategies that worked well in 2020 may not be reliable in 2023. As market conditions and geopolitical factors evolve, companies must reassess their transportation and customs processes to be effective. Automakers are doing this now and finding success with certain strategies – like nearshoring.

Hedging against volatility

Nearshoring, reshoring, or friend-shoring is the process of relocating manufacturing operations closer to the final destination of the product. The strategy gained popularity when U.S.-China tariffs were established and made it increasingly difficult and expensive to import from specific regions.

Now, global shipping and political volatility is prompting many automakers to leverage this strategy to diversify their supply chain and reduce risk. To name a few, Volkswagen announced it’s establishing an EV plant in Canada and Tesla and BMW are establishing or growing plants in Mexico.

The idea of nearshoring is daunting and complex. For companies looking to assess whether it’s right for their operations, they should start by looking into their sourcing analysis report. Digging into this can help them understand sourcing shifts, trade agreements that vary by region, or other location factors that could impact the total landed cost of goods. Using a supply chain technology partner can help with developing this type of report.

Moving manufacturing operations doesn’t automatically lower shipping costs. Because of the complex global shipping environment and the state of supply chain infrastructure in any country, ground transportation can be equally as expensive as shipping containers across the ocean. Due to the complex ocean shipping environment this Spring, a truckload from Mexico to the U.S. could be more expensive than a container shipped from China. For many automakers, having fewer delays is worth a lot of money.

Understanding the overall cost of nearshoring requires a holistic look at the entire supply chain so the decision can be made with all variables considered.

Other things to consider

Of course, nearshoring alone isn’t the only way to save costs and manage risk in the supply chain. An updated customs audit can ensure that duties are only being paid on required products. Working with a trade expert when nearshoring can help assess if agreements such as USMCA have created any additional cost-saving opportunities to consider. Moving to Mexico, for example, allows qualifying products to be transported duty-free under USMCA.

Demurrage and detention costs rose dramatically for global shippers over the Covid-19 pandemic, so it’s important to factor those in when considering nearshoring. Among top automakers, it wasn’t uncommon to exceed logistics budgets by up to 200% due to high fuel costs, shipping rates and dwell times. Managing container prioritization and consolidation offerings for truckload and ocean can both minimize delays and storage costs. So, while it may be more expensive to ship via truck instead of ocean container to the U.S., factoring in demurrage and detention costs may show that shifting some of your freight to utilize truckload can lead to cost savings. Overall, being flexible with modes and a mix of contractual and spot pricing can help amid market uncertainty.

Agility is still key

The events of the last few years have demonstrated the importance of an agile supply chain. The automakers that want to keep up with growing demand will need to use strategies that allow them to quickly adjust to market conditions. Nearshoring can help reduce costs and delivery risks, but no single manufacturing location or shipping mode can protect against disruption. Working with supply chain partners can help with understanding the varying risks, costs, and opportunities that come with shipping in the post-pandemic global environment.