Descartes Systems Group, the global leader in uniting logistics-intensive businesses in commerce, released its March Global Shipping Report for logistics and supply chain professionals. In February 2024, U.S. container import volumes declined 6% from January, but jumped 23.3% when compared to the same month last year. We would expect the month-over-month results to be smaller as February is a shorter month. The year-over-year results would indicate exceptional growth; however, they do not take into account the impact of the Chinese Lunar New Year on the February 2023 results. The growth is still strong but, based upon Descartes’ analysis, it is more likely to be ~13%, which is further explained below.

Compared to January 2024, imports from China reversed their robust growth in February, which impacted West Coast ports—especially the Port of Long Beach. Lower import volumes benefitted port transit delays as the combination of the Panama drought and Middle East conflict had less impact at the top East and Gulf Coast ports. The March update of the logistics metrics Descartes is tracking shows that 2024 is starting off to be a strong year for U.S. container imports; however, global supply chain performance may be impacted throughout the year because of ongoing conditions at the Panama and Suez Canals and upcoming labor negotiations at U.S. South Atlantic and Gulf Coast ports.

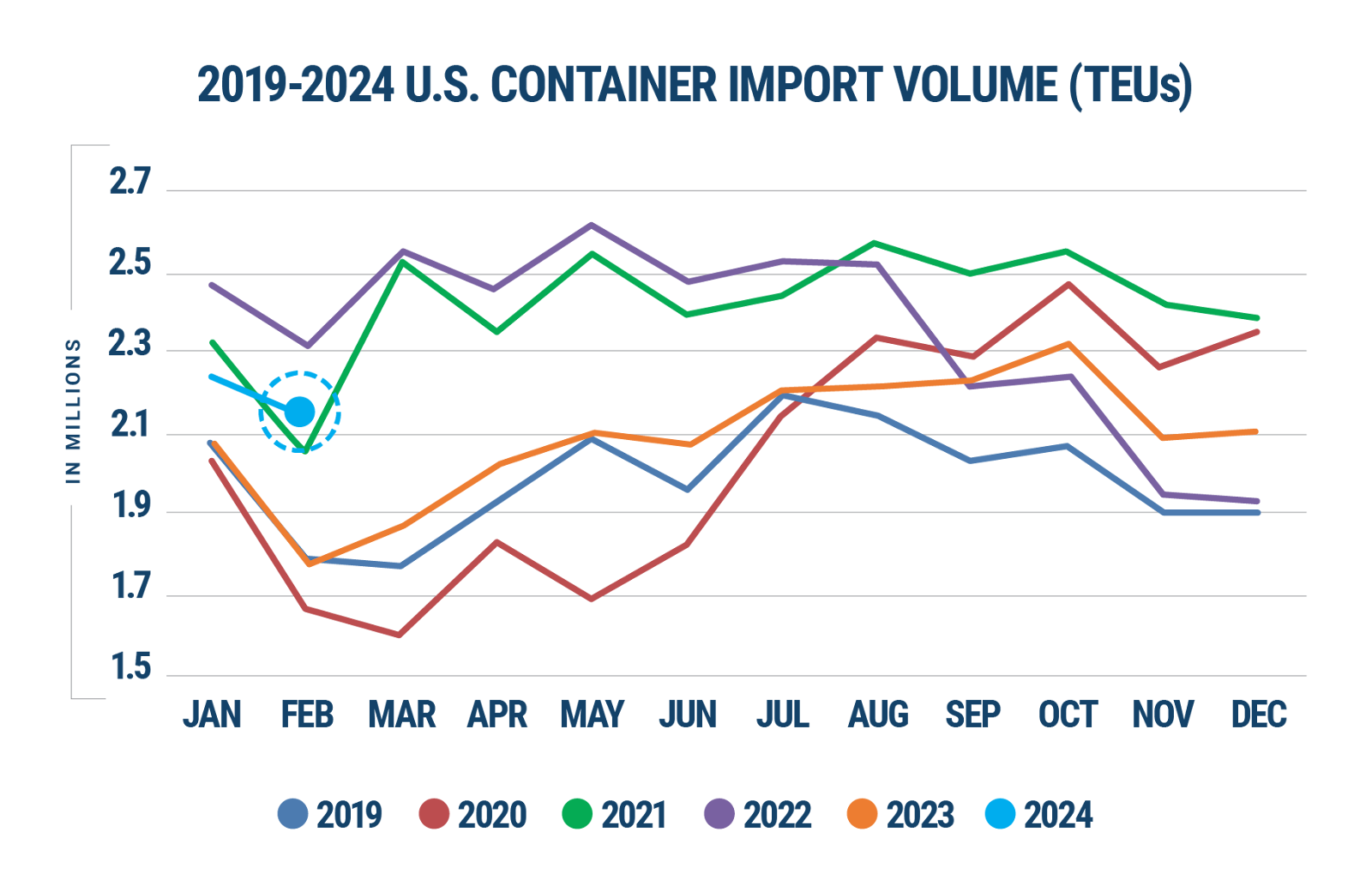

U.S. container imports show strong growth.

February 2024 U.S. container import volumes decreased 6.0% from January 2024 to 2,137,724 twenty-foot equivalent units (TEUs) (see Figure 1). Versus February 2023, TEU volume was higher by 23.3%, and up 19.5% from pre-pandemic February 2019. There are several reasons for the sharp year-over-year increase that could overstate this February’s results. Leap year occurred in 2024, adding one day of capacity in February. In addition, Chinese Lunar New Year occurred on February 11 this year versus January 22 in 2023, so February 2024 saw no impact on U.S. imports from China while February 2023 did. To gain more clarity on the year-over-year performance, Descartes analyzed TEU volumes for the first 15 days in February of both years where there would be no impact from Chinese Lunar New Year. During this timeframe, the growth in container imports was 13.3%, which is much more representative. Overall, Figure 1 shows that the first two months of 2024 are more in line with the consumer-fueled pandemic growth.

Source: Descartes Datamyne™

“February 2024 was a strong month considering its brevity and continues the robust performance that started in January 2024,” said Chris Jones, EVP Industry and Services, Descartes. “The combined effect of the Panama drought and the conflict in the Middle East on transit times declined in February and volume for the Gulf Coast ports remained constant versus January.”

The March report is Descartes’ thirty-first installment since beginning its analysis in August 2021. To read past reports, learn more about the key economic and logistics factors driving global shipping performance, and review strategies to help minimize global shipping challenges, visit Descartes’ Global Shipping Resource Center.